Discover everything about India’s official digital currency – the e₹. Learn how the digital rupee works, how to use it for daily payments, its benefits, safety, differences from UPI & crypto, and the future of CBDC in India.

Introduction: India’s Financial Future Goes Digital

India, a country known for leapfrogging into the digital era through innovations like UPI and Aadhaar, is now witnessing the dawn of another major financial milestone—the Digital Rupee (e₹). Introduced by the Reserve Bank of India (RBI), this Central Bank Digital Currency (CBDC) represents a new way to handle money: entirely virtual, government-backed, and accessible to everyone—from high-tech urbanites to remote rural villagers.

With a vision to reduce cash dependency, promote financial inclusion, and modernize payment systems, e₹ has emerged as a game-changer. But what exactly is this digital currency? How does it differ from UPI, and why is it important? This comprehensive guide explores how the e₹ works, how you can use it, and what it means for India in 2025.

What Is the Digital Rupee (e₹)?

The Digital Rupee, or e₹, is a digital representation of India’s official fiat currency. Unlike cryptocurrencies such as Bitcoin or Ethereum, which are decentralized and volatile, the digital rupee is issued, regulated, and backed entirely by the RBI. It is legal tender, meaning it can be used just like cash to settle any kind of transaction in the country.

The RBI has ensured that 1 e₹ is always equivalent to 1 physical rupee. What makes the digital rupee revolutionary is that it doesn’t need a traditional bank account. It operates through special digital wallets developed and authorized by the RBI, making it possible for people to transact securely even without a bank or internet connection in some cases. This is especially beneficial for India’s large unbanked and underbanked population, offering a leap toward greater financial inclusion.

How e₹ Differs From UPI and Mobile Wallets

At first glance, it may appear similar to digital payment methods like UPI (Unified Payments Interface) or mobile wallets such as PhonePe and Paytm. However, there’s a fundamental difference. UPI transactions are just interbank transfers; money is moved from one bank account to another via a third-party app. These transactions require an internet connection, depend on banking infrastructure, and often involve intermediaries.

In contrast, e₹ functions as a digital equivalent of cash. It is transferred directly from one wallet to another without involving any banks in real-time. Since it is issued by the RBI, it doesn’t depend on the banking system for verification, thus enabling instant settlements. Moreover, the e₹ can function offline, a feature that gives it a major edge in remote areas where internet connectivity is poor or unavailable.

Types of Digital Rupee in India

The RBI has implemented the Digital Rupee in two main formats to serve distinct purposes: Retail (e₹-R) and Wholesale (e₹-W).

The Retail e₹ (e₹-R) is designed for use by the general public—individuals and small businesses. It can be used for daily payments like groceries, utility bills, school fees, and shopping. It is currently being tested in pilot programs across select Indian cities and is gaining traction due to its simplicity and efficiency.

On the other hand, the Wholesale e₹ (e₹-W) is meant for institutions such as banks, stock exchanges, and large corporations. This form is used for interbank transfers, government bond settlements, and high-value financial transactions. By eliminating intermediaries and reducing transaction time, the wholesale digital rupee enhances the speed and security of India’s financial backbone.

Pilot Programs and Expansion Timeline

The digital rupee was officially launched in pilot mode in December 2022, starting with a few selected banks including State Bank of India (SBI), ICICI Bank, HDFC Bank, and YES Bank. The initial rollout focused on Tier 1 cities like Mumbai, Delhi, Bengaluru, and Bhubaneswar. Over time, it expanded to include over 50 cities, with new regions being added monthly as part of the RBI’s phased strategy.

Feedback from the pilot program has been largely positive. Users appreciated the seamless transaction experience, the reduced dependency on internet connectivity, and the low transaction time. One standout feature has been the offline mode, which enables transactions in areas with low or no network. This could prove to be revolutionary for financial inclusion in India’s rural and hilly regions.

How the Digital Rupee Works

To understand the digital rupee’s workflow, imagine converting your ₹500 in your bank account into a digital ₹500 in your e₹ wallet. This transaction is recorded directly with the RBI, and the amount is stored in your mobile wallet—independent of any bank. From there, you can spend it at any merchant that accepts e₹, transfer it to another individual’s wallet, or even use it to pay bills or recharge services.

The process begins with downloading an RBI-authorized wallet app, often provided by participating banks. Users register using their mobile number or Aadhaar. After verification, they receive a CBDC wallet linked to the RBI’s secure servers. Users can load money into the wallet using UPI, NEFT, or via QR cash deposits at specific counters. Once the wallet is loaded, payments can be made by scanning QR codes or entering wallet IDs, just like other digital wallets—but with no intermediary delays or bank charges.

How to Use e₹ in Daily Life

In everyday life, the digital rupee can be used just like physical currency but in a more convenient form. From buying vegetables at the local market to paying for metro rides, the application of e₹ is vast and growing. Schools and educational institutions have started accepting e₹ for fee payments, while some state governments are looking to deliver subsidies and benefits directly into e₹ wallets, removing the need for bank-based transfers.

E-commerce platforms and utility service providers are also integrating e₹ payment gateways. With time, it is expected that even street vendors and rural artisans will adopt e₹, given its ease of use and accessibility, especially in offline mode.

Is the Digital Rupee Safe?

Yes, safety is one of the key advantages of the digital rupee. Since it is regulated directly by the RBI, every transaction is logged securely, and wallets are encrypted with advanced cybersecurity protocols. The RBI has adopted a blockchain-inspired Distributed Ledger Technology (DLT), ensuring transparency, immutability, and protection against hacking or fraud.

Users are authenticated through multi-factor mechanisms, including biometric data and OTPs. Unlike traditional wallets which rely on private companies and bank APIs, the e₹ system is embedded with government-level encryption, making it one of the safest digital money systems in the world today.

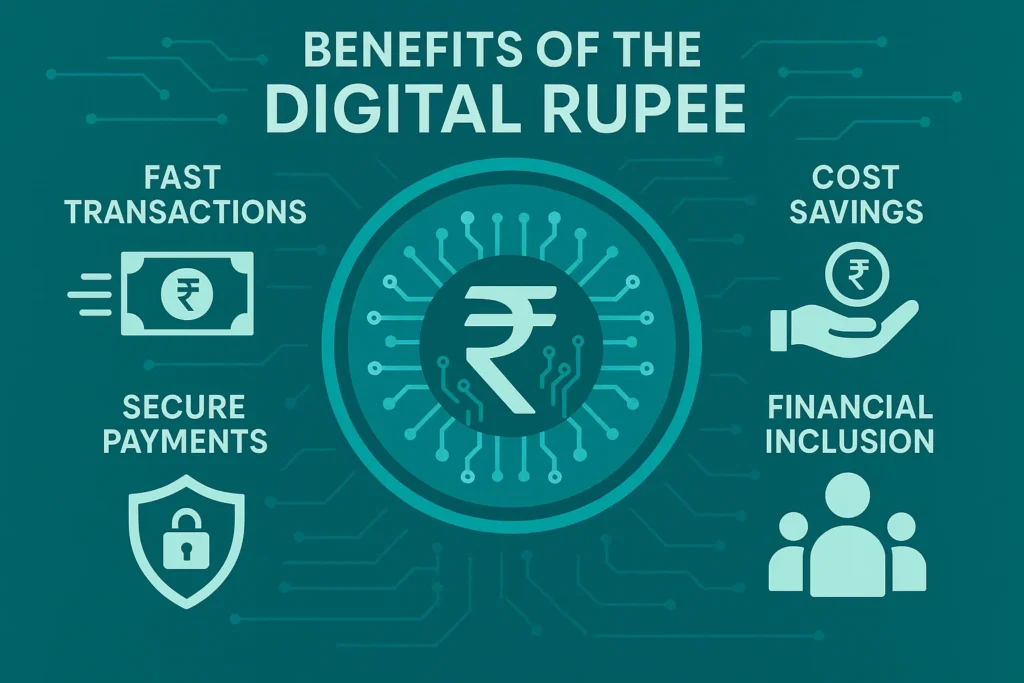

Benefits of the Digital Rupee

The digital rupee brings numerous benefits to individuals, businesses, and the government. For citizens, it means instant, zero-fee transactions, reduced dependency on cash, and access to modern financial tools even without a bank account. For businesses, it offers faster settlement, no POS charges, and better bookkeeping. For the government, e₹ ensures complete traceability, reduces corruption, and drastically cuts costs associated with printing and managing physical cash.

With e₹’s offline capability, even those living in internet-dark zones can now participate in digital finance. This opens up massive opportunities for economic empowerment and access to government schemes.

Challenges and Concerns

While promising, the e₹ ecosystem is not without its challenges. The biggest concern for many is privacy. Since the government technically has access to all transactions, there are worries about surveillance and data misuse. The RBI has stated it will protect user data and is working on ensuring anonymity for small transactions, but widespread adoption will depend on public trust.

Another challenge is user adoption, especially among older generations or those in rural areas who still prefer physical cash. Education, awareness campaigns, and incentives will be critical to ensuring the transition is smooth. Lastly, the success of the offline feature—currently in the testing phase—will play a big role in ensuring nationwide accessibility.

Digital Rupee vs Cryptocurrency

It is essential to differentiate between the digital rupee and cryptocurrencies. While both are digital in nature, they are fundamentally different. The e₹ is centralized, stable, and backed by the government. Cryptocurrencies are decentralized, highly volatile, and unregulated in India.

Whereas crypto like Bitcoin is seen as an investment or speculative asset, e₹ is intended as legal currency for everyday use. It offers all the benefits of digital money—convenience, speed, cost-efficiency—without the risks associated with crypto markets.

Economic and Social Impact of e₹

The introduction of the digital rupee could significantly impact India’s economic landscape. By enabling real-time, cost-free financial transactions, productivity across industries can increase. More transparent transactions can reduce black money circulation and increase tax compliance, boosting public revenue.

On the social front, it empowers individuals by granting access to formal financial systems. From migrant workers sending money home to small businesses receiving payments without delays, e₹ can act as an equalizer. It also supports India’s broader goal of becoming a cashless economy and strengthens its global position in fintech innovation.

Getting Started With e₹ in 2025

Getting started with e₹ is easier than ever. Most major banks, including SBI, ICICI, HDFC, and YES Bank, offer their own CBDC wallet apps. You can download these apps from the Play Store or App Store. After a simple KYC process, your wallet becomes active. Load money using UPI or a bank account and start transacting digitally—no bank visits required. The RBI is also working with telecom companies to introduce SIM-based e₹ services for feature phone users, making it accessible even to those without smartphones.

What the Future Holds for Digital Rupee

The future of the digital rupee looks bright. The RBI is planning to enable cross-border payments using e₹ in collaboration with other countries launching their own CBDCs. This could simplify remittances for NRIs and boost foreign trade. Other planned features include e₹ ATMs, biometric authentication, and even smart contracts using e₹ in sectors like insurance and real estate.

With the government’s continued push for Digital India and the fintech ecosystem maturing rapidly, e₹ is poised to become an integral part of our financial lives in the next few years.

Conclusion: Should You Use the Digital Rupee?

The digital rupee is more than a payment tool—it’s a paradigm shift in how money is managed, used, and perceived. With its advantages of speed, security, and simplicity, along with RBI’s backing, it provides an excellent alternative to cash and current digital wallets. Whether you’re a student looking to buy books online, a farmer receiving subsidies, or a small shopkeeper collecting payments, e₹ offers a powerful, secure, and future-ready option.

The shift may take time, and challenges remain, but if implemented effectively, the digital rupee could become the backbone of India’s digital economy. So yes, now is the time to explore and embrace the e₹ for more info about India’s Digital Rupee (e₹) click here